Whitewater City Manager Kevin Brunner recently touted an A2 rating from Moody’s Investor Services. It’s what he didn’t say that’s most telling.

In his January 15th Weekly Report, Whitewater City Manager Kevin Brunner announced an affirmation from Moody’s Investor Services of the city’s A2 bond rating. The city’s rating is assigned to the sale of million dollars in bonds, of two different types. The bonds are public debt, that the city must repay with interest. Brunner included the Moody’s announcement, with his own preface, in his weekly report.

Here are my remarks, with the full announcement from Brunner appearing at the bottom of this post, for reference.

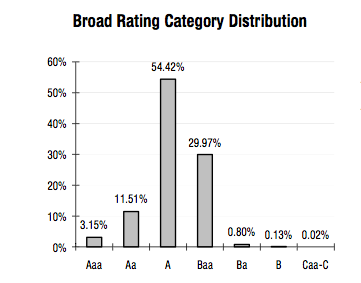

Moody’s rating of ‘A’ is actually a common rating — over half of municipalities rated have received it over a thirty-year period.

The A2 rating that Whitewater received (as re-affirmation) isn’t exceptional — it’s common. Moody’s rates municipal bond investments on a broad category scale as follows: Aaa, Aa, A, Baa, Ba, and so on. Within a category, such as ‘A,’ there’s additional differentiation between A1, A2, etc.

In the thirty-year period between 1970 and 2000, of the municipal bond investments Moody’s rated, over 54% were rated as ‘A.’ That’s right — over half. It’s hardly an exceptional rating — ‘A’ is the most common rating as a broad category across an entire generation of Moody’s ratings. See, Moody’s US Municipal Bond Rating Scale.

Here’s Moody’s own distribution chart, reproduced as Fair Use commentary:

Whitewater’s in the middle, with a rating like most others. It’s certainly not exemplary.

Not only that, but Whitewater’s investments received an A2 rating, less than some others (that is, A1) within the most common category of ratings. We’re in the middle of the middle, so to speak — no better than typical.

That’s how Whitewater rated, but the Whitewater city manager’s announcement tells nothing of the the commonplace nature of the rating. On the contrary, one would think that the city had won some sort of prestigious honor.

Even a steak sauce does better:

There’s a habit in Whitewater to insist that pig’s ears are silk purses. No bother trying to make one from the other – here insistence alone is enough.

Moody’s — receives compensation for any solicited rating — only unsolicited ratings require no payment to Moody’s.

There’s much that has been written about the benefits and risks of solicited and unsolicited sets of ratings. Of this one can say with certainty that where the rating is solicited, the firm has received compensation for its services, but gains access to records it requests. Where the rating is unsolicited, the firm rates without financial interest, but bases the rating only on public information.

A solicited, and supposedly objective analysis in these issues comes for a price; the success of an issue may depend on the rating. Everybody involved in these transactions knows as much.

The bond rating depends most on the city’s ability to repay the bond issue with interest. Analyses of the actual conditions of residents are secondary to the ability of the city to tax to repay the debt with interest.

In this regard, Brunner’s like a man who buys a pricey suit and assumes that the purchase proves he’s in good health. There is, of course, more room to tax – after all, it was Brunner who recently proposed an increase in the tax levy, in the middle of a deep recession, until Common Council saw better than to heap burdens on the city’s residents. Residents would have been worse off if he had his way.

Moody’s analysis shows how much Whitewater depends on the university, rather than city-sponsored projects, for its stability and survival.

Even a casual glance at the Moody’s report — and Brunner must have done as much — reveals that Moody’s fundamentally bases its rating on the obvious truth that

city’s economy is dominated by the University of Wisconsin-Whitewater campus. While the associated property is tax-exempt and consequently unavailable as a taxable resource, Moody’s believes that the stability and employment opportunities that it affords local residents are significant positive credit factors. The university is by far the largest employer with over 1,000 employees and enrollment has hit a record level of approximately 11,000 students. The school continues to expand and, as evidence, has recently opened a new business school and residence halls this fall. In 2008 the value of the city’s building permits swelled due to a $30 million university construction project.

These aren’t accomplishments of city government — the campus props up the town. I’ve argued as much for years. The City of Whitewater may thank the State of Wisconsin for whatever opportunity we have. These are not accomplishments of the city’s politicians and bureaucrats.

The rating’s analysis shows that we lag Wisconsin and America.

Both Madison and Milwaukee — even Milwaukee, with all her troubles – have higher ratings. Whitewater’s median family income trails Wisconsin, and unemployment is over the state average. No mention of child poverty, by the way — a figure that would not be affected by the presence of students (the presence of which Moody’s uses as an excuse to explain Whitewater’s below-average income statistics.)

Our rate of child poverty is astonishingly high — about one in four children. A taxpayer funded tech park that relies on a taxpayer-funded agency as an anchor tenant will do nothing for them.

The rating ignores alternatives to borrowing.

Understandably, Moody’s merely reviews if the city can pay back a multi-million obligation, even if it has to tax more to do so. I am sure that there is more to take from common residents — even the Sheriff of Nottingham could find an additional farthing or two from some ordinary person in Sherwood Forest.

There’s no analysis of whether this is the right plan and course for Whitewater. The alternatives to the plan of a few middling bureaucrats’ vain ambitions to gobble as much stimulus money as possible, with additional debt heaped on the city as a result, are beyond Moody’s scope.

About Whitewater’s “successful use of tax increment districts (TIDs), including five additional TIDs established in 2007…”

Did someone write Moody’s analysis on April 1st? It’s not even a suitable fool’s day joke. If all the tax incremental districts were so successful, why would city manager Brunner bother to write, in his preface to his proposed 2010 budget, that “I also want the Finance Director to evaluate possible city debt savings through restructuring/refinancing. This will be especially critical in the next few months if the distressed TID legislation is approved by the State Legislature as expected and we will be look at how TID #4 could be extended beyond its current life.”

Moody’s analyst, you might want to call 911: Whitewater TID 4 may need a defibrillator, a distressed TID bill, something…

The local press coverage of the bond rating.

One can see an unquestioning view of public officials over at a local newspaper. (Too funny, especially, is Brunner going on about how it would be unrealistic to expect the rating to be higher. Well, he’s right about at least one thing.)

Ultimately, crowing over a commonplace rating, and ignoring the very words that show Whitewater lags behind, serves not Whitewater, but advances only one bureaucrat’s overweening vanity.

From the city manager’s Weekly Report:

City Receives A2 Bond Rating for Upcoming Borrowing for Technology Park Development

Earlier this week, Moody’s Investor Services issued the following report on the city’s finances and continued to assign an A2 rating to the city bond issues that are scheduled for sale next Tuesday. Given the current economy and municipal financial difficulties, maintaining existing bond ratings can be difficult with a number of downgrades and only a very few upgrades occurring. Reading the report is very interesting and provides a good objective review of our community and its financial condition.

NEW YORK, January 13, 2010 —

Moody’s Investors Service has assigned an A2 rating to the City of Whitewater’s (WI) $3.3 million Taxable General Obligation Community Development Bonds, which will be offered as Build America Bonds, and $2.1 million General Obligation Refunding Bonds. Concurrently, Moody’s has affirmed the A2 rating on the city’s outstanding general obligation debt affecting $14.1 million. Both the taxable and tax-exempt bonds are secured by the city’s general obligation unlimited tax pledge. The community development bonds will finance infrastructure improvements within the city’s technology park (tax increment financing district four). The tax-exempt bonds will refinance three state loans and two privately placed loans for a net present value savings. The A2 rating reflects the city’s sound financial position, stable local economy significantly anchored by a state university, and manageable debt profile.

LOCAL ECONOMY DOMINATED BY STATE UNIVERSITY EXPECTED TO REMAIN STABLE

Whitewater is favorably located 45 miles southeast of Madison (general obligation rated Aaa/stable outlook) and 55 miles southwest of Milwaukee (rated Aa2/negative outlook). The city’s economy is dominated by the University of Wisconsin-Whitewater campus. While the associated property is tax-exempt and consequently unavailable as a taxable resource, Moody’s believes that the stability and employment opportunities that it affords local residents are significant positive credit factors. The university is by far the largest employer with over 1,000 employees and enrollment has hit a record level of approximately 11,000 students. The school continues to expand and, as evidence, has recently opened a new business school and residence halls this fall. In 2008 the value of the city’s building permits swelled due to a $30 million university construction project.

The city’s tax base is moderately-sized at $639 million, though this excludes the university campus, and growth over the last five years has been somewhat measured, averaging 5.1% increases annually. The city has encouraged diversity and growth through the successful use of tax increment districts (TIDs), including five additional TIDs established in 2007. Wealth indices are skewed downward given the presence of the large student population which accounts for 78% of the population. While the per capita income figures reflect the impact of the substantial student population (65.7% of the state average), the median family income is much stronger at 91.1% of the state average. Walworth County’s (general obligation rated Aa2) unemployment rate of 7.8% in October 2009 was slightly higher that than of the state and nation.

SOUND FINANCIAL POSITION SUPPORTED BY CONSERVATIVE MANAGEMENT

Moody’s expects the city to maintain a sound financial position due to prudent management evidenced by relatively healthy reserves. Over the last five years, the city has maintained essentially balanced operations with the exceptions of fiscal 2004 and 2008. In fiscal 2004, the city drew down its reserves by $584,000 due to a one time expenditure of $623,770 to retire the city’s unfunded pension liability. In fiscals 2005, 2006 and 2007 the city’s General Fund balance remained stable at $2.5 million, equal to 29.5% of fiscal 2007revenues. The city realized a deficit of $197,000 in fiscal 2008 due to higher than expected expenditures related to snow and ice removal early in the year and flood clean-up over the summer. While the city did receive about $100,000in Federal Emergency Management Agency (FEMA) reimbursement, the funds did not cover the entire out-of-pocket amount spent by the city. Officials report that fiscal 2009 year-end results will likely reflect a slight deficit of up to$68,000, though a portion of this is expected to be offset by unspent contingency funds. The city had budgeted the use of about $68,500 in reserves in fiscal 2009 to meet operational costs. Notably, the city did not implement any staff reductions or furloughs. In fiscal 2010 the city’s state shared revenue is expected to decline by $68,000, the city reduced its General Fund levy, and $75,000 of General Fund reserves were applied to the budget. Favorably, over $90,000 was budgeted as a contingency expenditure (equal to 1% of the budget) and, due to unused taxing margin year after year, the city can roll forward about $360,000. Although the city applies a modest amount of reserves to the budget each year, management expects to adhere to its General Fund balance policy of maintaining a minimum of 20% of the subsequent year’s budget.

In addition to property taxes, which account for 26.8% of the city’s fiscal 2008 operational revenue, the city receives a portion of its operational revenue from state shared utility revenue. Since the property valuation of aco-generation facility, constructed and operated by LS Power (senior secured rated Baa3/stable outlook), is not included in the city’s tax base, the utility pays tax on gross receipts to the state and the state subsequently makes annual payments to the city based on the valuation of the utility’s assets. Payments of $750,000 began in 1997 and will continue in lesser amounts going forward. Payments are tied to the depreciated value of the facility and therefore will decline slightly through 2012 and remain stable thereafter. The city has chosen to use these funds to pay debt service and cash finance capital projects, in order to preserve structural fiscal balance between recurring revenues and recurring expenditures.

MANAGEABLE DEBT POSITION GIVEN SIGNIFICANT SUPPORT FROM NON-DEBT SERVICE LEVY SOURCES

Moody’s expects the city’s above average debt burden will remain manageable given significant support from non-debt service levy sources and rapid principal amortization of 100% in ten years. The city’s direct debt burden is elevated at 3.1% of full valuation as is its overall debt burden of 4.4%. The city’s general obligation debt service is heavily supported by the revenues from the LS Power co-generation facility and increment from the city’s TIDs which together cover over 80% of the city’s debt service. Management plans to issue a series of refinancing bonds later this year for savings but has no capital borrowing plans until 2011 or 2012.

KEY STATISTICS

2008 Population estimate: 14,291 (6.4% increase since 2000)

2009 Full value: $639 million

Estimated full value per capita: $44,717

Direct Debt: 3.1%

Overlapping Debt: 4.4%

Fiscal 2008 General Fund Balance: $2.3 million (26.6% of revenues)

Walworth County’s unemployment rate (10/09): 7.8%

2000 Per capita income as a % of state: 65.7% (64.7% of US)

2000 Median family income as a % of state: 91.1% (96.3% of US)

Post-sale GOULT debt outstanding: $19.6 million

The principal methodology used in rating the current issue was Moody’s General Obligation Bonds Issued by U.S. Local Governments, published in October 2009 and available on www.moodys.com in the Rating Methodologies sub-directory under the Research & Ratings tab. Other methodologies and factors that may have been considered in the process of rating this issuer can also be found in the Rating Methodologies sub-directory on Moody’s website. The last rating action was on July 28, 2009 when the A2 GOULT rating for the city was affirmed.